We talked about control variate in [4]: when evaluating ![\mathbb{E}_{p(x)}[f(x)]](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-c90b259513baa02e344aa8367f8c223d_l3.png "Rendered by QuickLaTeX.com") by Monte Carlo samples, we can instead evaluate

by Monte Carlo samples, we can instead evaluate ![\mathbb{E}_{p(x)}[f(x)-h(x)+\theta]](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-b13a4b8be64daf2c070d7f4c57fd8a3a_l3.png "Rendered by QuickLaTeX.com") with

with ![\theta=\mathbb{E}_{p(x)}[h(x)]](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-a8de21a662a2a66494d54b9acdc51880_l3.png "Rendered by QuickLaTeX.com") in order to reduce variance. The requirement for control variate to work is that

in order to reduce variance. The requirement for control variate to work is that  is correlated with

is correlated with  and the mean of is known.

and the mean of is known.

In this post we will walk through a classic example of using control variate, in which is picked as the Taylor expansion of . We know that ‘s Taylor expansion can be expressed as  . Therefore, if we pick the second order of Taylor expansion for and set

. Therefore, if we pick the second order of Taylor expansion for and set  , we get

, we get  .

.

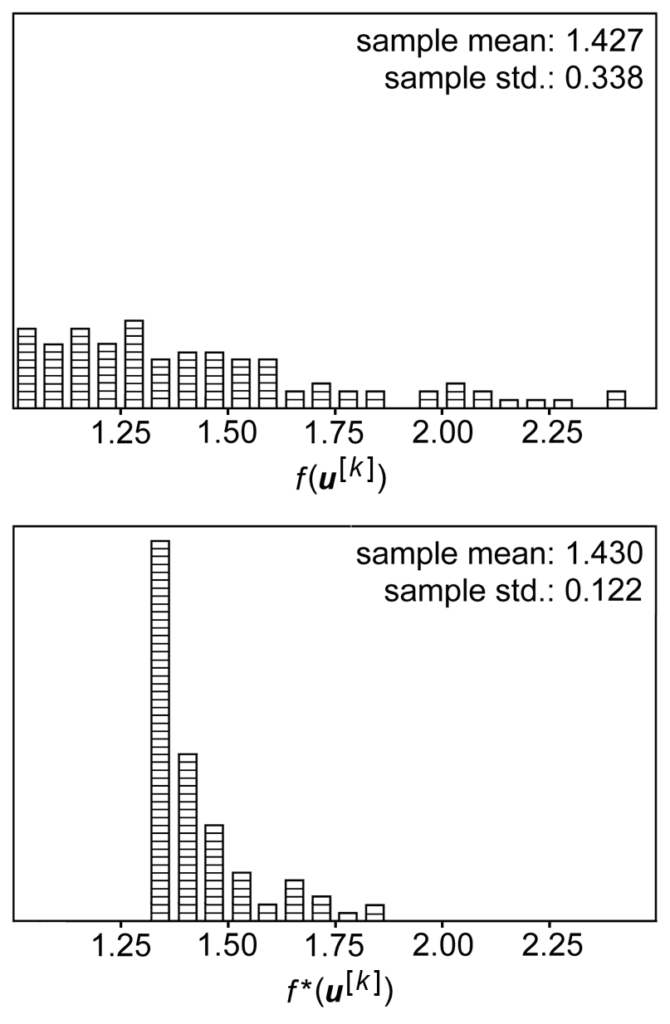

Let’s see an example from [6]. Suppose ![f(u_1, u_2)=exp[(u_1^2 + u_2^2)/2]](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-f69a56e44acd47bc30c23e01cc063e79_l3.png "Rendered by QuickLaTeX.com") and we want to evaluate the integral

and we want to evaluate the integral  . If we want to use Monte Carlo estimator to estimate

. If we want to use Monte Carlo estimator to estimate  using

using  samples, we have:

samples, we have:

The control variate as the second-order Taylor expansion of is  (we use multi-variable Taylor expansion here [7]). We first compute its mean:

(we use multi-variable Taylor expansion here [7]). We first compute its mean: ![\theta=\mathbb{E}_{p(x)}[h(x)] = \int^1_0\int^1_0 \left(1 +(u_1^2+u_2^2)/2 \right) du_1 du_2 = 4/3](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-78f185df22133a668d294ba879d7e49f_l3.png "Rendered by QuickLaTeX.com") . Thus, our control variate Monto Carlo estimator is:

. Thus, our control variate Monto Carlo estimator is:![\frac{1}{m}\sum\limits_{k=1}^{m} z(u_1, u_2)\newline=\frac{1}{m}\sum\limits_{k=1}^{m} \left[f(u_1, u_2) -h(u_1, u_2) + \theta\right]\newline=\frac{1}{m}\sum\limits_{k=1}^{m} \left[exp[(u_1^2 + u_2^2)/2] - 1 - (u_1^2 + u_2^2)/2 + 4/3 \right]](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-cefe400b6090655af28e4c28735815f6_l3.png "Rendered by QuickLaTeX.com") .

.

And from the results of [6] the sampling variance of  is smaller than

is smaller than  .

.

Now what [2] propose is to apply similar Taylor expansion-based control variate on REINFORCE policy gradient:

![\nabla_\theta J(\theta) = \mathbb{E}_{s_t \sim \rho_{\pi}(\cdot), a_t \sim \pi(\cdot | s_t)} \left[ \nabla_\theta log \pi_\theta (a_t | s_t) R_t\right]](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-837adae19f5b171b2c9a7a93a089f8ff_l3.png "Rendered by QuickLaTeX.com")

If we use Monte Carlo estimator, then we essentially use samples  to approximate

to approximate  , which causes variance. If we have a control variate

, which causes variance. If we have a control variate  and

and  can be chosen at any value but a sensible choice being

can be chosen at any value but a sensible choice being  , a deterministic version of

, a deterministic version of  , then the control variate version of policy gradient can be written as (Eqn. 7 in [2]):

, then the control variate version of policy gradient can be written as (Eqn. 7 in [2]):![\nabla_\theta log \pi_\theta(a_t | s_t) R_t - h(s_t, a_t) + \mathbb{E}_{s\sim \rho_\pi, a \sim \pi}\left[ h(s_t, a_t)\right] \newline=\nabla_\theta log \pi_\theta(a_t | s_t) R_t - h(s_t, a_t) + \mathbb{E}_{s \sim \rho_\pi}\left[ \nabla_a Q_w(s_t, a)|_{a=\mu_\theta(s_t)} \nabla_\theta \mu_\theta(s_t)\right]](https://czxttkl.com/wp-content/ql-cache/quicklatex.com-9629b8ff4fc66089624196ff0d65190c_l3.png "Rendered by QuickLaTeX.com")

As you can see the second term can be computed when  is some critic with known analytic expression, and actually does not depend on

is some critic with known analytic expression, and actually does not depend on  .

.

[3] uses the law of total variance (some good examples and intuitions [8, 9]) to decompose the control-variate policy gradient into three parts: variance caused by variance of states  , variance of actions

, variance of actions  , and variance of trajectories

, and variance of trajectories  . What [3] highlights is that the magnitude of is usually greatly smaller than the rest two so the benefit of using control variate-based policy gradient is very limited.

. What [3] highlights is that the magnitude of is usually greatly smaller than the rest two so the benefit of using control variate-based policy gradient is very limited.

References

[1] MUPROP: UNBIASED BACKPROPAGATION FOR STOCHASTIC NEURAL NETWORKS

[2] Q-PROP: SAMPLE-EFFICIENT POLICY GRADIENT WITH AN OFF-POLICY CRITIC

[3] The Mirage of Action-Dependent Baselines in Reinforcement Learning

[4] https://czxttkl.com/2020/03/31/control-variate/

[5] https://czxttkl.com/2017/03/30/importance-sampling/

[6] https://www.value-at-risk.net/variance-reduction-with-control-variates-monte-carlo-simulation/

[7] https://en.wikipedia.org/wiki/Taylor_series#Taylor_series_in_several_variables

[8] http://home.cc.umanitoba.ca/~farhadi/ASPER/Law%20of%20Total%20Variance.pdf