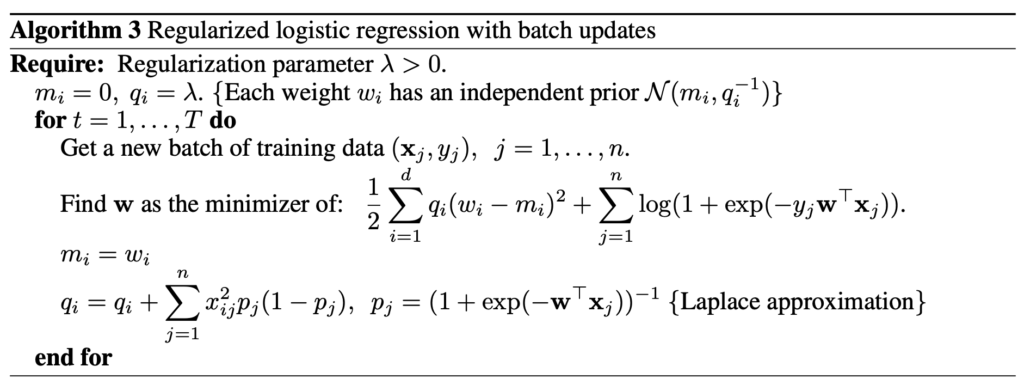

Recently, I am studying a basic contextual bandit algorithm called Logistic Regression Bandit, which is also known as Bayesian Logistic Regression. It all starts from the paper “An Empirical Evaluation of Thompson Sampling” [1]. In Algorithm 3 in the paper, the authors gives the pseudo-code for how to train the Logistic Regression Bandit, assuming its weights are from a Gaussian distribution with a diagonal covariance matrix:

When I first read it, my biggest confusion is Laplace approximation – why is it used in training a Bayesian logistic regression? Now, let’s dig into how Laplace approximation comes into play.

Let’s first review the set up of a Bayesian logistic regression. Suppose we have a feature space  . We have a dataset

. We have a dataset  which contains tuples of

which contains tuples of  for

for  . These are observed features and labels. If we apply a Bayesian logistic regression on such data, the logistic regression will have a weight vector of the same dimension as the features:

. These are observed features and labels. If we apply a Bayesian logistic regression on such data, the logistic regression will have a weight vector of the same dimension as the features:  . The prediction function is a sigmoid function:

. The prediction function is a sigmoid function:  .

.

Because it is a Bayesian logistic regression, we need to estimate a posterior probability distribution for  given the observation ,

given the observation ,  . We assume that come from a multi-dimensional Gaussian distribution with a diagonal covariance matrix. This is the same as what Algorithm 3’s notation implies:

. We assume that come from a multi-dimensional Gaussian distribution with a diagonal covariance matrix. This is the same as what Algorithm 3’s notation implies:  .

.

We can also get the likelihood function

Using the Bayesian Theorem, we can derive (the notations adapted from [2] (slides page 9~12) to the notations in this post):

Now, here is how Lapalace Approximation [3] comes into play. The goal of Lapalace Approximation is to learn a Gaussian distribution to approximate , which is not a Gaussian distribution in its exact expression. In other words, if  , what would be

, what would be  and

and  ?

?

First, we will take the logarithm on both sides, leading to:

Suppose  achieves maximum

achieves maximum  , which is able to be found using gradient ascent or expressed in a closed formula (I think is a concave function but not totally sure). Based on the 2nd-order Taylor expansion at point , we have:

, which is able to be found using gradient ascent or expressed in a closed formula (I think is a concave function but not totally sure). Based on the 2nd-order Taylor expansion at point , we have:  . Because

. Because  , we can further simplify to

, we can further simplify to  .

.

can actually be seen as the logarithm of another Gaussian distribution

can actually be seen as the logarithm of another Gaussian distribution  , whose mean is at and variance as

, whose mean is at and variance as  , and

, and  absorbs any remaining constants. This is why Algorithm 3 updates

absorbs any remaining constants. This is why Algorithm 3 updates  because

because  is essentially from that maximizes , and

is essentially from that maximizes , and  since this is essentially

since this is essentially  .

.

To summarize, Laplace Approximation finds a new Gaussian distribution to approximate !

Reference

[1] An Empirical Evaluation of Thompson Sampling: https://papers.nips.cc/paper/2011/hash/e53a0a2978c28872a4505bdb51db06dc-Abstract.html

[2] https://cs.iupui.edu/~mdundar/CSCIMachineLearning/Lecture12.pdf

[3] https://bookdown.org/rdpeng/advstatcomp/laplace-approximation.html